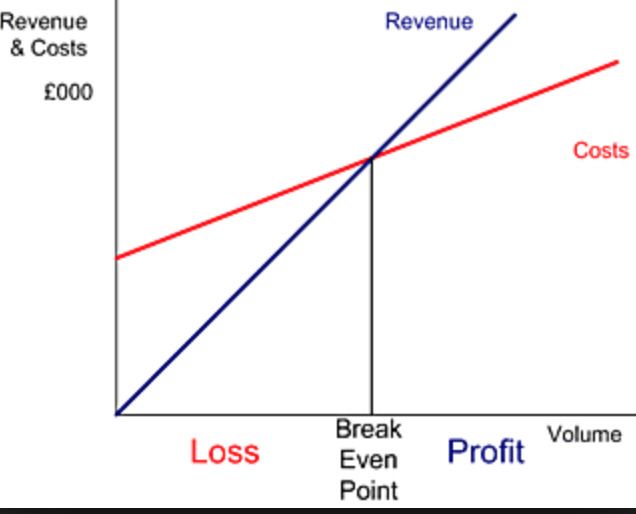

Every business has revenues and costs. When the revenues and costs are not aligned, the business sooner or later risks bankruptcy. Let me illustrate with a few examples.

A restaurant’s costs consist of raw food materials and labor. While the revenues are a function of the amount of food sold. So, in case the revenue falls, the cost of labor kills the restaurant business. A cloud kitchen, due to its reduced labor costs, is more resilient. The costs of oil (or mining) companies consist of drilling and transportation. While the revenue is a strong function of the unpredictable oil/mineral price. That’s why small oil and mining companies go out of business whenever there is a sharp fall in the price of the commodity sold. An airline’s costs consist primarily of the predictable cost of leasing the airplanes and the unpredictable oil prices to fly the plane. While the revenue consists of the number of seats sold well in advance. So, any fall in seats sold or any sudden spikes in oil prices leads to a disaster. A software company’s costs consist mostly of labor and infrastructure. While the revenue comes from the increased sales of the software. The incremental cost of serving a user is marginal, while the fixed costs are huge. That’s why landing a few big initial contracts to become default-alive can make a huge difference in the long run. An exchange takes a cut of transactions flowing through it. The costs and revenues are aligned. Further, if it is an electronic exchange, like stock exchanges or Ad exchanges, then the infrastructural costs are minimal and employee costs are less material. This becomes a pure money-making exercise.